Once a city has laid a strong fiscal foundation, it can begin making smart investments that improve the quality of life and increase prosperity. This is the fun part: public spaces that draw crowds, policies that attract and create new businesses, and programs that improve residents’ lives. But to be worth it, those investments must return more value than they cost.

Growth can be a great thing for city finances. But what happens when that growth slows or stops altogether? A downturn in the housing market, a factory closure, or a sudden drop in sales tax revenue can bring city budgets under stress. When that happens, can your city still meet its obligations to taxpayers and lenders?

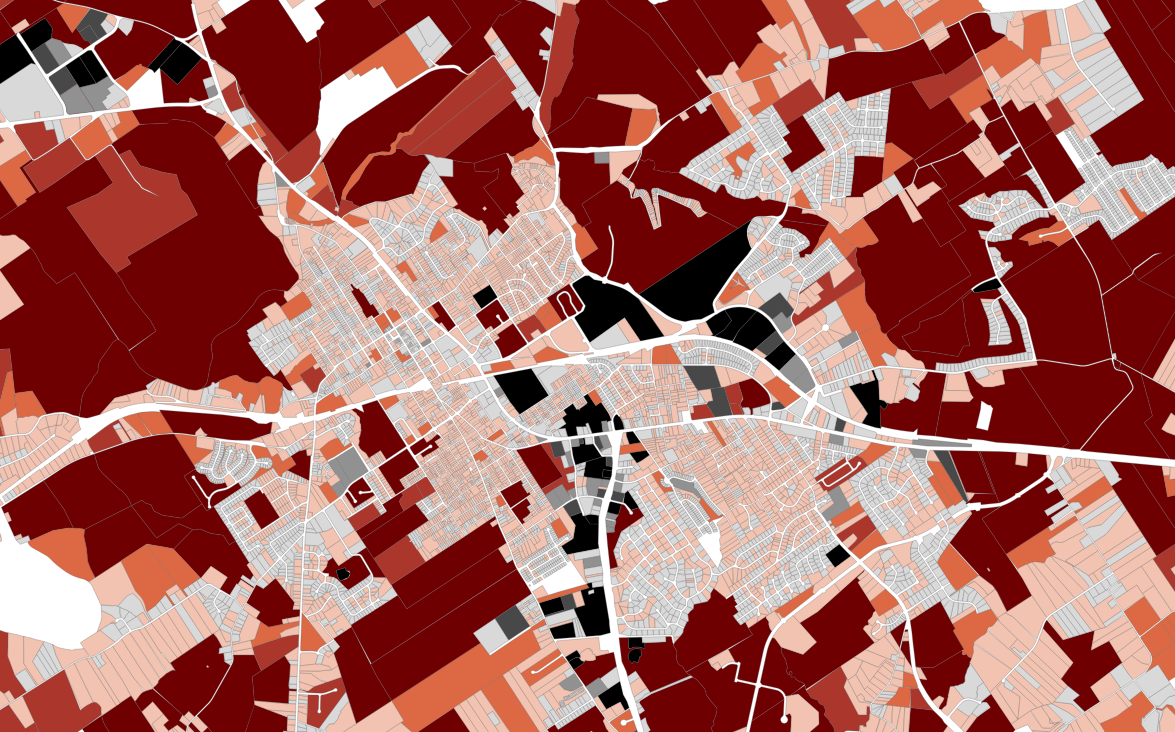

This week, we are taking a look at the role of land use plans in achieving a city’s wants and needs. Every city council member, town planner, and resident has an idea of what they want their city to be. With this vision in mind, they draft a land use plan to facilitate what they like and keep out what they don’t. However, these plans often treat fundamental needs as an afterthought, making it more difficult for the city to fulfill its obligations. Putting needs first instead will ultimately give cities greater flexibility to pursue their wants down the road.